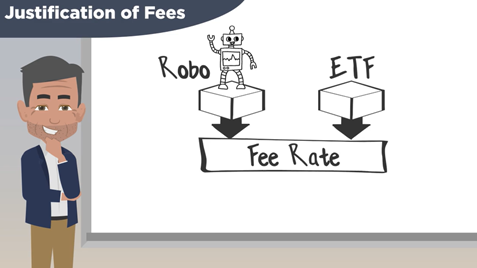

I was honored to participate in Addepar’s Discovery Week back in June, alongside Amy DeTolla of Focus Financial and Cameron Sheehan of Addepar. During our session, we covered many topics including trends affecting our industry and how to most easily evaluate your firm’s technology needs to make smarter decisions. One question Cameron posed to me was about changes to advisor compensation — namely, had I witnessed the fee compression that is often written about in industry publications due to the onslaught of low-cost robo advisors and/or ETFs. After briefly pondering the question, my answer was a resounding, “No, I haven’t witnessed large-scale fee compression across our industry, despite many doomsday predictions.” While my answer was factually correct, that response taken at face value isn’t fully transparent – you need to dig a bit deeper to fully understand the underlying condition.

While the average fee rate in the RIA industry has stayed around 77 basis points according to the reports I continue to see (on a sliding scale, with larger portfolios typically paying less and smaller portfolios typically paying more), that’s not to say they stayed at that level with no downward pressure from robo advisors or low-cost ETFs. There has definitely been pressure, but thanks to tremendous hard work by the advisory community, that pressure hasn’t resulted in actual compression of fees.

Source: The COO Society; Key Performance Indicators course, Business Administration Learning Path

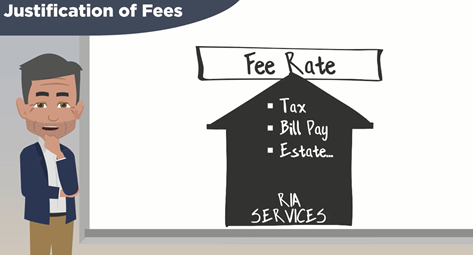

By adding additional services to their traditional offering of asset allocation and investment management for liquid assets, advisors have been able to explain to clients that their AUM fee encompasses much more, thus keeping their fee level the same. Clients are now receiving access to alternative investments; comprehensive financial planning is now included as part of the AUM fee being charged; many firms are now offering trust and estate planning, bill pay services, and in some cases, RIAs are now processing tax returns on behalf of their clients. There clearly has been downward pressure, with clients asking, “What am I getting for the fee I pay you?” Advisors, in my opinion, have done a great job in articulating the full value of those fees, and thus justifying their worth to their clients.

Source: The COO Society; Key Performance Indicators course, Business Administration Learning Path

While these additional services have kept the average fee rate from clients constant, these new services cost money, thus putting downward pressure on profit margins. These new service offerings require additional employees and, in many cases, require additional technology tools. These services are also tougher to scale than asset allocation models that can be executed through trading and rebalancing software. Therefore, if an RIA kept revenue from existing clients the same, but added additional costs to service those clients, we’d have a problem.

Fortunately, these additional services have done more than simply justify fees to existing clients – with more arrows in their service offering quiver, firms have been able to add additional clients, and in many cases, these clients have been larger than the clients traditionally serviced by the RIA. This makes sense – larger, more complex clients will be looking for help with estate planning, bill pay, access to non-traditional asset classes, etc. With these services now part of the marketing efforts of the firm, more prospective clients should now be attracted to it. And once they hire the RIA, with so much of their financial lives being catered to, the assets should be stickier than simple “investment-only” clients.

Kevin Hrdlicka of Savant Wealth Management discussed this phenomenon on Episode 30 of The COO Roundtable podcast. Over time, Savant has added tax services, retirement planning, they own an accounting and payroll firm and have recently affiliated with a law firm to draft estate documents. Kevin feels these additional services not only have made the clients stickier to the firm and justified their fee rates over time, but he’s tracked the average client size and has watched that increase in step with the addition of these additional services. He said, “We’ve all seen that service expansion to maintain the fee, but our goal is really to be a one-stop shop for all aspects of a client’s financial life, beyond just investment management.”

My short answer to Cameron’s question about fee compression was correct – in general, RIAs have not seen fees drop precipitously due to low-cost robo advisors and ETFs – but that’s not to say advisors can get complacent. The only reason we haven’t seen fee compression is because firms have pivoted to offering more services in order to justify those fees. Without an uptick in the number of clients served and the average size of those clients getting larger thanks to these additional services, RIAs could find themselves in a precarious situation. Business owners must always remember that profit margins are quite literally the bottom line when it comes to their business. Additional services can justify fees to clients, but RIA owners must also justify those services to themselves by tracking their margins. These additional services should be touted loudly in the firm’s marketing campaigns to attract new (and hopefully larger) clients. It’s the compression of margins, and not necessarily fees, that owners should be tracking.